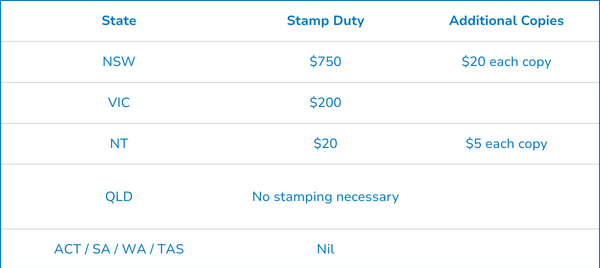

Generally, the establishment of a trust deed will be subject to either nil or nominal duty. The requirements in relation to stamping a trust deed vary from state to state. The stamping fees for discretionary and unit trusts, if by declaration/settlement of cash only are set out below:

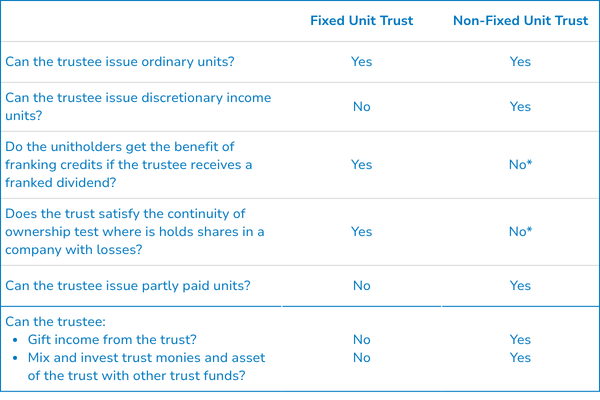

There are a number of issues you should take into account in choosing between a fixed and a non-fixed unit trust. The key differences are sumarised below:

*Unless the trust lodges a family trust election

Recent cases also highlight the fact that most private unit trusts do not meet the current criteria for a fixed trust – therefore if you have an existing unit trust deed, you may need to update it if you require the trust to be fixed.

A fixed trust is more restrictive than our ordinary unit trust, which may be a problem if there are non-arm’s length unitholders.

For example, many decisions have to be approved by a unanimous resolution of unitholders (e.g. amendments to the trust deed).

Recent cases also indicate that, unless unit redemptions and issues have to be based on a valuation determined on a net asset basis and in accordance with Australian accounting principles, the unitholders may not have a fixed entitlement.

While we do not agree with the recent case law, it is likely the ATO will seek to take this valuation position and therefore the safest option is to include these valuation methods in the unit trust deed.

The deed can be amended in future (by unanimous consent) if an alternative valuation method is agreed.